On Feb. 6, 2018, the stock market officially entered “correction” territory. A stock market correction is defined as a drop of at least 10% or more for an index or stock from its recent high. [1] During one week the stock data prices (closed price) were decreasing for many stocks. Are there any signals that can be used to predict next stock market correction?

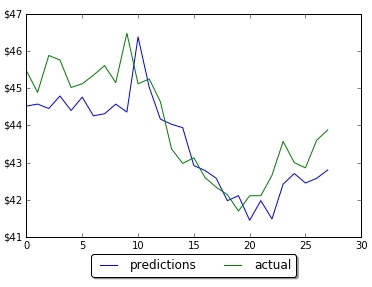

I pulled historical data from 20 stocks selected randomly and then created python program that counts how many stocks (closed price) were decreased, increased or did not change for each day (comparing with previous day). The numbers then converted into percentage. So if all 20 stock closed prices decreased at some day it would be 100%. For now I was just looking at % of decreased stocks per day. Below is the graph for decreasing stocks. Highlighted zone A is when we many decreasing stocks during the correction.

Observations

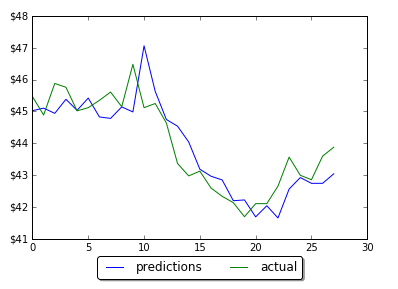

I did not find good strong signal to predict market correction but probably more analysis needed. However before this correction there was some increasing trend for number of stocks that close at lower prices. This is shown below. On this graph the trend line can be viewed as indicator of stock market direction.

Python Source Code to download Stock Data

Here is the script that was used to download data:

from pandas_datareader import data as pdr

import time

# put below actual symbols as many as you need

symbols=['XXX','XXX', 'XXX', ...... 'XXX']

def get_data (symbol):

data = pdr.get_data_google(symbol,'1970-01-01','2018-02-19')

path="C:\\Users\\stocks\\"

data.to_csv( path + symbol+".csv")

return data

for symbol in symbols:

get_data(symbol)

time.sleep(7)

Script for Stock Data Analysis

Here is the program that takes downloaded data and counts the number of decreased/increased/same stocks per day. The results are saved in the file and also plotted. Plots are shown after source code below.

And here is the link to the data output from the below program.

# -*- coding: utf-8 -*-

import os

path="C:\\Users\\stocks\\"

from datetime import datetime

import pandas as pd

import numpy as np

def days_between(d1, d2):

d1 = datetime.strptime(d1, "%Y-%m-%d")

d2 = datetime.strptime(d2, "%Y-%m-%d")

print (d1)

print (d2)

return abs((d2 - d1).days)

i=10000 # index to replace date

j=20 # index for stock symbols

k=5 # other attributes

data = np.zeros((i,j,k))

symbols=[]

count=0

# get index of previous trade day

# because there is no trades on weekend or holidays

# need to calculate prvious trade day index instead

# of just subracting 1

def get_previous_ind(row_ind, col_count ):

k=1

print (str(row_ind) + " " + str(col_count))

while True:

if data[row_ind-k][col_count][0] == 1:

return row_ind-k

else:

k=k+1

if k > 1000 :

print ("ERROR: PREVIOUS ROW IS NOT FOUND")

return -1

dates=["" for i in range(10000) ]

# read the entries

listOfEntries = os.scandir(path)

for entry in listOfEntries:

if entry.is_file():

print(entry.name)

stock_data = pd.read_csv (str(path) + str(entry.name))

symbols.append (entry.name)

for index, row in stock_data.iterrows():

ind=days_between(row['Date'], "2002-01-01")

dates[ind] = row['Date']

data[ind][count][0] = 1

data[ind][count][1] = row['Close']

if (index > 1):

print(entry.name)

prev_ind=get_previous_ind(ind, count)

delta= 1000*(row['Close'] - data[prev_ind][count][1])

change=0

if (delta > 0) :

change = 1

if (delta < 0) :

change = -1

data[ind][count][3] = change

data[ind][count][4] = 1

count=count+1

upchange=[0 for i in range(10000)]

downchange=[0 for i in range(10000)]

zerochange=[0 for i in range(10000)]

datesnew = ["" for i in range(10000) ]

icount=0

for i in range(10000):

total=0

for j in range (count):

if data[i][j][4] == 1 :

datesnew[icount]=dates[i]

total=total+1

if (data[i][j][3] ==0):

zerochange[icount]=zerochange[icount]+1

if (data[i][j][3] ==1):

upchange[icount]=upchange[icount] + 1

if (data[i][j][3] == - 1):

downchange[icount]=downchange[icount] + 1

if (total != 0) :

upchange[icount]=100* upchange[icount] / total

downchange[icount]=100* downchange[icount] / total

zerochange[icount]=100* zerochange[icount] / total

print (str(upchange[icount]) + " " + str(downchange[icount]) + " " + str(zerochange[icount]))

icount=icount+1

df=pd.DataFrame({'Date':datesnew, 'upchange':upchange, 'downchange':downchange, 'zerochange':zerochange })

print (df)

df.to_csv("changes.csv", encoding='utf-8', index=False)

import matplotlib.pyplot as plt

downchange=downchange[icount-200:icount]

upchange=upchange[icount-200:icount]

zerochange=zerochange[icount-200:icount]

# Two subplots, the axes array is 1-d

f, axarr = plt.subplots(3, sharex=True)

axarr[0].plot(downchange)

axarr[0].set_title('downchange')

axarr[1].plot(upchange)

axarr[1].set_title('upchange')

axarr[2].plot(zerochange)

axarr[2].set_title('zerochange')

plt.show()

References

1. 6 Things You Should Know About a Stock Market Correction

2. How to Predict the Eventual Stock Market Correction Before Anyone Else

3. 4 Ways To Predict Market Performance

You must be logged in to post a comment.