As stated on allstarcharts.com by expert with more than 10 years, Fibonacci Analysis is one of the most valuable and easy to use tools for stock market technical analysis. And Fibonacci tools can be applied to longer-term as well as to short-term. [3]

In this post we will take a look how Fibonacci numbers can help to stock market analysis. For this we will use different daily stock prices data charts with added Fibonacci lines.

Just for the references – The Fibonacci numbers (or Fibonacci sequence), are numbers that after the first two are the sum of the two preceding ones[1] : 0, 1, 1, 2, 3, 5, 8, 13, 21, 34, 55 …

According to “Magic of Fibonacci Sequence in Prediction of Stock Behavior” [7] Fibonacci series are widely used in financial market to predict the resistance and support levels through Fibonacci retracement. In this method major peak and trough are identified, then it is followed by dividing the vertical distance into 23.6%, 38.2%, 50%, 61.8% and 100%. These percentage numbers (except 50%) are obtained by dividing element in Fibonacci sequence by its successors for example 13/55=0.236. [2]

Ratio of two successive numbers of Fibonacci sequence is approximately 1.618034, so if we multiply 23.6 by 1.618034 we will get next level number 38.2.

5 Fibonacci Chart Examples

Now let’s look at charts with added Fibonacci lines (23.6%, 38.2%, 50%, 61.8% and 100%).

Below are 5 daily the stock market price charts for different stock tickers. Fibonacci line numbers are shown on the right side, and stock ticker is on the top of chart.

Botz stock data chart with Fibonacci lines

Here we can see Fibonacci line at 61.8 is a support line

Botz stock data chart with Fibonacci lines

This chart is for the same symbol but for smaller time frame. 23.6 line is support and then resistance line

GE stock data chart with Fibonacci lines

Here are Fibonacci Retracement lines at 23.6 and 61.8 line up well with support and resistance areas

GE stock data chart with Fibonacci lines

Fibonacci Retracement 61.8 is support line

T stock data chart with Fibonacci lines

Fibonacci Retracement lines such as 23.6, 38.2, 61.8 line up well with support and resistance areas

Conclusion

After reviewing above charts we can say that Fibonacci Retracement can indicate potential support and resistance levels. The trend often is changing in such areas. So Fibonacci retracement can be used for stock market prediction.

Do you use Fibonacci tools? Feel free to put in the comments how do you apply Fibonacci retracements in stock trading. Do you find Fibonacci tools helpful or not? As always any feedback is welcome.

Can sweet food affect our mood? A friend of mine was interesting if some of his minor mood changes are caused by sugar intake from sweets like cookies. He collected and provided records and in this post we will use correlation data analysis with python pandas dataframes to check the connection between food and mood. We will create python script for this task.

From internet resources we can confirm that relationship between how we feel and what we eat exists.[1] Sweet food is not recommended to eat as fluctuations in blood sugar cause mood swings, lack of energy [2]. The information about chocolate is however contradictory. Chocolate affects us both negatively and positively.[3] But chocolate has also sugar.

What if we eat only small amount of sweets and not each day – is there still any connection and how strong is it? The machine learning data analysis can help us to investigate this.

The Problem

So in this post we will estimate correlation between sweet food and mood based on provided daily data. Correlation means association – more precisely it is a measure of the extent to which two variables are related. [4]

Data

The dataset has two columns, X and Y where: X is how much sweet food was taken on daily basis, on the scale 0 – 1 , 0 is nothing, 1 means a max value. Y is variation of mood from optimal state, on the scale 0 – 1 , 0 – means no variations or no defects, 1 means a max value.

Approach

If we calculate correlation between 2 columns of daily data we will get something around 0. However this would not show whole picture. Because the effect of the food might take action in a few days. The good or bad feeling can also stay for few days after the event that caused this feeling.

So we would need to take average data for several days for both X (looking back) and Y (looking forward). Here is the diagram that explains how data will be aggregated:

Changing the data – averaging

And here is how we can do this in the program:

1.for each day take average X data for last N days and take average Y data for M next days.

2.create a pandas dataframe which has now new moving averages for X and Y.

3.calculate correlation between new X and Y data

What should be N and M? We will use different values – from 1 to 14. And we will check what is the highest value for correlation.

Here is the python code to use pandas dataframe for calculating averages:

def get_data (df_pandas,k,z):

x = np.zeros(df_pandas.shape[0])

y = np.zeros(df_pandas.shape[0])

new_df = pd.DataFrame() #creates a new dataframe that's empty

for index, row in df_pandas.iterrows():

x[index]=df_pandas.loc[index-k:index,'X'].mean()

y[index]=df_pandas.loc[index:index+z,'Y'].mean()

new_df=pd.concat([pd.DataFrame(x),pd.DataFrame(y)], "columns")

new_df.columns = ['X', 'Y']

return new_df

Correlation Data Analysis

For calculating correlation we use also pandas dataframe. Here is the code snipped for this:

for i in range (1,n):

for j in range (1,m):

data=get_data(df, i, j)

corr_df.loc[i, j] = data['X'].corr(data['Y'])

print ("corr_df")

print (corr_df)

pandas.DataFrame.corr by default is calculating pearson correlation coefficient – it is the measure of the strength of the linear relationship between two variables. In our code we use this default option. [8]

Results

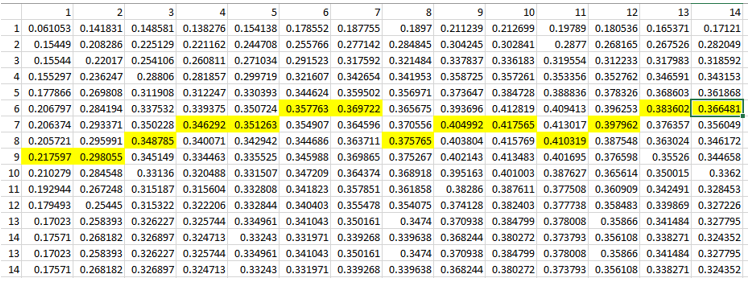

After calculating correlation coefficients we output data in the table format and plot results on heatmap using seaborn module. Below is the data output and the plot. The max value of correlation for each column is highlighted in yellow in the data table. Input data and full source code are available at [5],[6].

Correlation data between sweet food (taken in n days) and mood (in next m days)Correlation data between sweet food (taken in N days) and mood in the following M days, averaged

Conclusion

We performed correlation analysis between eating sweet food and mental health. And we confirmed that in our data example there is a moderate correlation (0.4). This correlation is showing up when we use moving averaging for 5 or 6 days. This corresponds with observation that swing mood may appear in several days, not on the same or next day after eating sweet food.

We also learned how we can estimate correlation between two time series variables X, Y.

Neural networks are among the most widely used machine learning techniques.[1] But neural network training and tuning multiple hyper-parameters takes time. I was recently building LSTM neural network for prediction for this post Machine Learning Stock Market Prediction with LSTM Keras and I learned some tricks that can save time. In this post you will find some techniques that helped me to do neural net training more efficiently.

1. Adjusting Graph To See All Details

Sometimes validation loss is getting high value and this prevents from seeing other data on the chart. I added few lines of code to cut high values so you can see all details on chart.

import matplotlib.pyplot as plt

import matplotlib.ticker as mtick

T=25

history_val_loss=[]

for x in history.history['val_loss']:

if x >= T:

history_val_loss.append (T)

else:

history_val_loss.append( x )

plt.figure(6)

plt.plot(history.history['loss'])

plt.plot(history_val_loss)

plt.title('model loss adjusted')

plt.ylabel('loss')

plt.xlabel('epoch')

plt.legend(['train', 'test'], loc='upper left')

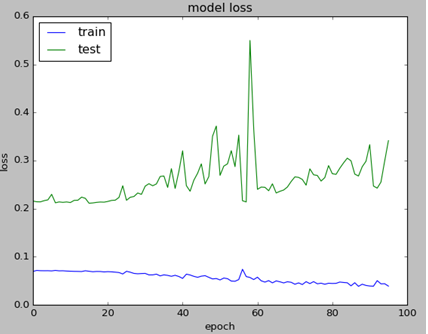

Below is the example of charts. Left graph is not showing any details except high value point because of the scale. Note that graphs are obtained from different tests. LSTM NN Training Value Loss Charts with High Number and Adjusted

2. Early Stopping

Early stopping is allowing to save time on not running tests when a monitored quantity has stopped improving. Here is how it can be coded:

Here is what arguments mean per Keras documentation [2].

min_delta: minimum change in the monitored quantity to qualify as an improvement, i.e. an absolute change of less than min_delta, will count as no improvement.

patience: number of epochs with no improvement after which training will be stopped.

verbose: verbosity mode.

mode: one of {auto, min, max}. In min mode, training will stop when the quantity monitored has stopped decreasing; in max mode it will stop when the quantity monitored has stopped increasing; in auto mode, the direction is automatically inferred from the name of the monitored quantity.

3. Weight Regularization

Weight regularizer can be used to regularize neural net weights. Here is the example.

I found that beta_1=0.89 performed better then suggested 0.91 or other tested values.

5. Rolling Window Size

Rolling window (in case we use it) also can impact on performance. Too small or too big will drive higher validation loss. Below are charts for different window size (N=4,8,16,18, from left to right). In this case the optimal value was 16 which resulted in 81% accuracy.

LSTM Neural Net Loss Charts with Different N

I hope you enjoyed this post on different techniques for tuning hyper parameters. If you have any tips or anything else to add, please leave a comment below in the comment box.

Below is the full source code:

import numpy as np

import pandas as pd

from sklearn import preprocessing

import matplotlib.pyplot as plt

import matplotlib.ticker as mtick

from keras.regularizers import L1L2

fname="C:\\Users\\stock data\\GM.csv"

data_csv = pd.read_csv (fname)

#how many data we will use

# (should not be more than dataset length )

data_to_use= 150

# number of training data

# should be less than data_to_use

train_end =120

total_data=len(data_csv)

#most recent data is in the end

#so need offset

start=total_data - data_to_use

yt = data_csv.iloc [start:total_data ,4] #Close price

yt_ = yt.shift (-1)

print (yt_)

data = pd.concat ([yt, yt_], axis =1)

data. columns = ['yt', 'yt_']

N=16

cols =['yt']

for i in range (N):

data['yt'+str(i)] = list(yt.shift(i+1))

cols.append ('yt'+str(i))

data = data.dropna()

data_original = data

data=data.diff()

data = data.dropna()

# target variable - closed price

# after shifting

y = data ['yt_']

x = data [cols]

scaler_x = preprocessing.MinMaxScaler ( feature_range =( -1, 1))

x = np. array (x).reshape ((len( x) ,len(cols)))

x = scaler_x.fit_transform (x)

scaler_y = preprocessing. MinMaxScaler ( feature_range =( -1, 1))

y = np.array (y).reshape ((len( y), 1))

y = scaler_y.fit_transform (y)

x_train = x [0: train_end,]

x_test = x[ train_end +1:len(x),]

y_train = y [0: train_end]

y_test = y[ train_end +1:len(y)]

x_train = x_train.reshape (x_train. shape + (1,))

x_test = x_test.reshape (x_test. shape + (1,))

from keras.models import Sequential

from keras.layers.core import Dense

from keras.layers.recurrent import LSTM

from keras.layers import Dropout

from keras import optimizers

from numpy.random import seed

seed(1)

from tensorflow import set_random_seed

set_random_seed(2)

from keras import regularizers

from keras.callbacks import EarlyStopping

earlystop = EarlyStopping(monitor='val_loss', min_delta=0.0001, patience=80, verbose=1, mode='min')

callbacks_list = [earlystop]

model = Sequential ()

model.add (LSTM ( 400, activation = 'relu', inner_activation = 'hard_sigmoid' , bias_regularizer=L1L2(l1=0.01, l2=0.01), input_shape =(len(cols), 1), return_sequences = False ))

model.add(Dropout(0.3))

model.add (Dense (output_dim =1, activation = 'linear', activity_regularizer=regularizers.l1(0.01)))

adam=optimizers.Adam(lr=0.01, beta_1=0.89, beta_2=0.999, epsilon=None, decay=0.0, amsgrad=True)

model.compile (loss ="mean_squared_error" , optimizer = "adam")

history=model.fit (x_train, y_train, batch_size =1, nb_epoch =1000, shuffle = False, validation_split=0.15, callbacks=callbacks_list)

y_train_back=scaler_y.inverse_transform (np. array (y_train). reshape ((len( y_train), 1)))

plt.figure(1)

plt.plot (y_train_back)

fmt = '%.1f'

tick = mtick.FormatStrFormatter(fmt)

ax = plt.axes()

ax.yaxis.set_major_formatter(tick)

print (model.summary())

print(history.history.keys())

T=25

history_val_loss=[]

for x in history.history['val_loss']:

if x >= T:

history_val_loss.append (T)

else:

history_val_loss.append( x )

plt.figure(2)

plt.plot(history.history['loss'])

plt.plot(history.history['val_loss'])

plt.title('model loss')

plt.ylabel('loss')

plt.xlabel('epoch')

plt.legend(['train', 'test'], loc='upper left')

fmt = '%.1f'

tick = mtick.FormatStrFormatter(fmt)

ax = plt.axes()

ax.yaxis.set_major_formatter(tick)

plt.figure(6)

plt.plot(history.history['loss'])

plt.plot(history_val_loss)

plt.title('model loss adjusted')

plt.ylabel('loss')

plt.xlabel('epoch')

plt.legend(['train', 'test'], loc='upper left')

score_train = model.evaluate (x_train, y_train, batch_size =1)

score_test = model.evaluate (x_test, y_test, batch_size =1)

print (" in train MSE = ", round( score_train ,4))

print (" in test MSE = ", score_test )

pred1 = model.predict (x_test)

pred1 = scaler_y.inverse_transform (np. array (pred1). reshape ((len( pred1), 1)))

prediction_data = pred1[-1]

model.summary()

print ("Inputs: {}".format(model.input_shape))

print ("Outputs: {}".format(model.output_shape))

print ("Actual input: {}".format(x_test.shape))

print ("Actual output: {}".format(y_test.shape))

print ("prediction data:")

print (prediction_data)

y_test = scaler_y.inverse_transform (np. array (y_test). reshape ((len( y_test), 1)))

print ("y_test:")

print (y_test)

act_data = np.array([row[0] for row in y_test])

fmt = '%.1f'

tick = mtick.FormatStrFormatter(fmt)

ax = plt.axes()

ax.yaxis.set_major_formatter(tick)

plt.figure(3)

plt.plot( y_test, label="actual")

plt.plot(pred1, label="predictions")

print ("act_data:")

print (act_data)

print ("pred1:")

print (pred1)

plt.legend(loc='upper center', bbox_to_anchor=(0.5, -0.05),

fancybox=True, shadow=True, ncol=2)

fmt = '$%.1f'

tick = mtick.FormatStrFormatter(fmt)

ax = plt.axes()

ax.yaxis.set_major_formatter(tick)

def moving_test_window_preds(n_future_preds):

''' n_future_preds - Represents the number of future predictions we want to make

This coincides with the number of windows that we will move forward

on the test data

'''

preds_moving = [] # Store the prediction made on each test window

moving_test_window = [x_test[0,:].tolist()] # First test window

moving_test_window = np.array(moving_test_window)

for i in range(n_future_preds):

preds_one_step = model.predict(moving_test_window)

preds_moving.append(preds_one_step[0,0])

preds_one_step = preds_one_step.reshape(1,1,1)

moving_test_window = np.concatenate((moving_test_window[:,1:,:], preds_one_step), axis=1) # new moving test window, where the first element from the window has been removed and the prediction has been appended to the end

print ("pred moving before scaling:")

print (preds_moving)

preds_moving = scaler_y.inverse_transform((np.array(preds_moving)).reshape(-1, 1))

print ("pred moving after scaling:")

print (preds_moving)

return preds_moving

print ("do moving test predictions for next 22 days:")

preds_moving = moving_test_window_preds(22)

count_correct=0

error =0

for i in range (len(y_test)):

error=error + ((y_test[i]-preds_moving[i])**2) / y_test[i]

if y_test[i] >=0 and preds_moving[i] >=0 :

count_correct=count_correct+1

if y_test[i] < 0 and preds_moving[i] < 0 :

count_correct=count_correct+1

accuracy_in_change = count_correct / (len(y_test) )

plt.figure(4)

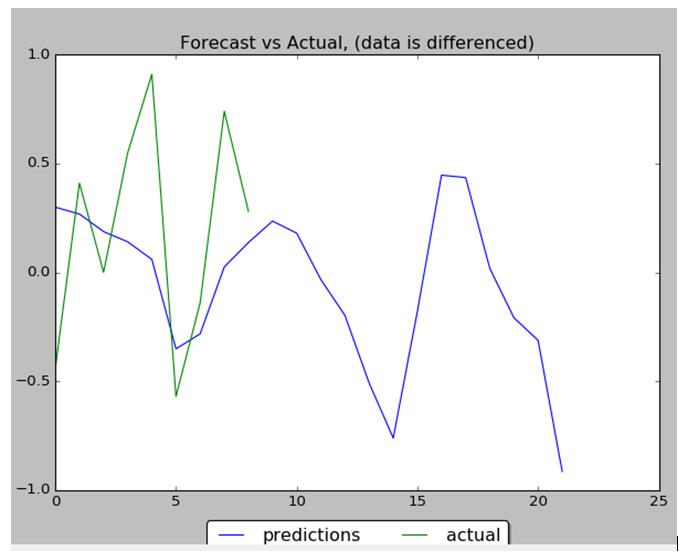

plt.title("Forecast vs Actual, (data is differenced)")

plt.plot(preds_moving, label="predictions")

plt.plot(y_test, label="actual")

plt.legend(loc='upper center', bbox_to_anchor=(0.5, -0.05),

fancybox=True, shadow=True, ncol=2)

print ("accuracy_in_change:")

print (accuracy_in_change)

ind=data_original.index.values[0] + data_original.shape[0] -len(y_test)-1

prev_starting_price = data_original.loc[ind,"yt_"]

preds_moving_before_diff = [0 for x in range(len(preds_moving))]

for i in range (len(preds_moving)):

if (i==0):

preds_moving_before_diff[i]=prev_starting_price + preds_moving[i]

else:

preds_moving_before_diff[i]=preds_moving_before_diff[i-1]+preds_moving[i]

y_test_before_diff = [0 for x in range(len(y_test))]

for i in range (len(y_test)):

if (i==0):

y_test_before_diff[i]=prev_starting_price + y_test[i]

else:

y_test_before_diff[i]=y_test_before_diff[i-1]+y_test[i]

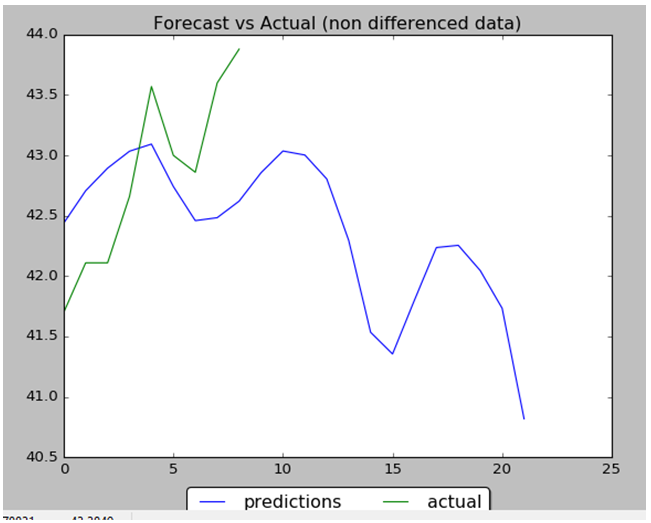

plt.figure(5)

plt.title("Forecast vs Actual (non differenced data)")

plt.plot(preds_moving_before_diff, label="predictions")

plt.plot(y_test_before_diff, label="actual")

plt.legend(loc='upper center', bbox_to_anchor=(0.5, -0.05),

fancybox=True, shadow=True, ncol=2)

plt.show()

In the previous posts [1,2] I created script for machine learning stock market price on next day prediction. But it was pointed by readers that in stock market prediction, it is more important to know the trend: will the stock go up or down. So I updated the script to predict difference between today and yesterday prices. If it is negative the stock price will go down, if positive it will go up. Below will be described implemented modifications.

Data inputting

Data from previous days are entered as features through additional columns. The number of columns can be changed through parameter N in the beginning of script. So for example for day 20 the input will contain data for day 21 as target and data for days 20, 19,18,17… 20-N

Also added differencing before scaling. Differencing helped to improve performance of network. It also makes easy to get changes from previous day. In the end the differenced data inverted back.

Below is the stock data prices after applying differencing (subtructing previous day stock data price from current day)

Stock Data Prices after Differencing

Predicting future changes

I used moving_test_window_preds function. Inside of this function the script within loop is adding new prediction to “moving window” array and removing first element from it. This is based on example from blog post on forecasting time series with LSTM[4].

So the script is predicting future day data based on the previous known data in the “moving window”, updating known data and starting again. The performance evaluated by comparing predicted data with test (not used before) data.

Weight regularization together with differencing helped to decrease overfitting.

Results

Performance of NN is 88% : 8 correct data out of 9. Below are the data charts that comparing predicted data (9 first days from 22 total days) with actual test data. Below you can find output chart and full python source code.

Stock Data Prices Prediction with LSTMStock Data Prices Prediction with LSTM, Data Inverted Back from Differencing

import numpy as np

import pandas as pd

from sklearn import preprocessing

import matplotlib.pyplot as plt

import matplotlib.ticker as mtick

from keras.regularizers import L1L2

fname="C:\\Users\\Leo\\Desktop\\A\\WS\\stock data analysis 2017\\GM.csv"

data_csv = pd.read_csv (fname)

#how many data we will use

# (should not be more than dataset length )

data_to_use= 150

# number of training data

# should be less than data_to_use

train_end =120

total_data=len(data_csv)

#most recent data is in the end

#so need offset

start=total_data - data_to_use

yt = data_csv.iloc [start:total_data ,4] #Close price

yt_ = yt.shift (-1)

print (yt_)

data = pd.concat ([yt, yt_], axis =1)

data. columns = ['yt', 'yt_']

N=18

cols =['yt']

for i in range (N):

data['yt'+str(i)] = list(yt.shift(i+1))

cols.append ('yt'+str(i))

data = data.dropna()

data_original = data

data=data.diff()

data = data.dropna()

# target variable - closed price

# after shifting

y = data ['yt_']

x = data [cols]

scaler_x = preprocessing.MinMaxScaler ( feature_range =( -1, 1))

x = np. array (x).reshape ((len( x) ,len(cols)))

x = scaler_x.fit_transform (x)

scaler_y = preprocessing. MinMaxScaler ( feature_range =( -1, 1))

y = np.array (y).reshape ((len( y), 1))

y = scaler_y.fit_transform (y)

x_train = x [0: train_end,]

x_test = x[ train_end +1:len(x),]

y_train = y [0: train_end]

y_test = y[ train_end +1:len(y)]

x_train = x_train.reshape (x_train. shape + (1,))

x_test = x_test.reshape (x_test. shape + (1,))

from keras.models import Sequential

from keras.layers.core import Dense

from keras.layers.recurrent import LSTM

from keras.layers import Dropout

from keras import optimizers

from numpy.random import seed

seed(1)

from tensorflow import set_random_seed

set_random_seed(2)

from keras import regularizers

model = Sequential ()

model.add (LSTM ( 400, activation = 'relu', inner_activation = 'hard_sigmoid' , bias_regularizer=L1L2(l1=0.01, l2=0.01), input_shape =(len(cols), 1), return_sequences = False ))

model.add(Dropout(0.3))

model.add (Dense (output_dim =1, activation = 'linear', activity_regularizer=regularizers.l1(0.01)))

adam=optimizers.Adam(lr=0.01, beta_1=0.89, beta_2=0.999, epsilon=None, decay=0.0, amsgrad=True)

model.compile (loss ="mean_squared_error" , optimizer = "adam")

history=model.fit (x_train, y_train, batch_size =1, nb_epoch =1400, shuffle = False, validation_split=0.15)

y_train_back=scaler_y.inverse_transform (np. array (y_train). reshape ((len( y_train), 1)))

plt.figure(1)

plt.plot (y_train_back)

fmt = '%.1f'

tick = mtick.FormatStrFormatter(fmt)

ax = plt.axes()

ax.yaxis.set_major_formatter(tick)

print (model.summary())

print(history.history.keys())

plt.figure(2)

plt.plot(history.history['loss'])

plt.plot(history.history['val_loss'])

plt.title('model loss')

plt.ylabel('loss')

plt.xlabel('epoch')

plt.legend(['train', 'test'], loc='upper left')

fmt = '%.1f'

tick = mtick.FormatStrFormatter(fmt)

ax = plt.axes()

ax.yaxis.set_major_formatter(tick)

score_train = model.evaluate (x_train, y_train, batch_size =1)

score_test = model.evaluate (x_test, y_test, batch_size =1)

print (" in train MSE = ", round( score_train ,4))

print (" in test MSE = ", score_test )

pred1 = model.predict (x_test)

pred1 = scaler_y.inverse_transform (np. array (pred1). reshape ((len( pred1), 1)))

prediction_data = pred1[-1]

model.summary()

print ("Inputs: {}".format(model.input_shape))

print ("Outputs: {}".format(model.output_shape))

print ("Actual input: {}".format(x_test.shape))

print ("Actual output: {}".format(y_test.shape))

print ("prediction data:")

print (prediction_data)

y_test = scaler_y.inverse_transform (np. array (y_test). reshape ((len( y_test), 1)))

print ("y_test:")

print (y_test)

act_data = np.array([row[0] for row in y_test])

fmt = '%.1f'

tick = mtick.FormatStrFormatter(fmt)

ax = plt.axes()

ax.yaxis.set_major_formatter(tick)

plt.figure(3)

plt.plot( y_test, label="actual")

plt.plot(pred1, label="predictions")

print ("act_data:")

print (act_data)

print ("pred1:")

print (pred1)

plt.legend(loc='upper center', bbox_to_anchor=(0.5, -0.05),

fancybox=True, shadow=True, ncol=2)

fmt = '$%.1f'

tick = mtick.FormatStrFormatter(fmt)

ax = plt.axes()

ax.yaxis.set_major_formatter(tick)

def moving_test_window_preds(n_future_preds):

''' n_future_preds - Represents the number of future predictions we want to make

This coincides with the number of windows that we will move forward

on the test data

'''

preds_moving = [] # Store the prediction made on each test window

moving_test_window = [x_test[0,:].tolist()] # First test window

moving_test_window = np.array(moving_test_window)

for i in range(n_future_preds):

preds_one_step = model.predict(moving_test_window)

preds_moving.append(preds_one_step[0,0])

preds_one_step = preds_one_step.reshape(1,1,1)

moving_test_window = np.concatenate((moving_test_window[:,1:,:], preds_one_step), axis=1) # new moving test window, where the first element from the window has been removed and the prediction has been appended to the end

print ("pred moving before scaling:")

print (preds_moving)

preds_moving = scaler_y.inverse_transform((np.array(preds_moving)).reshape(-1, 1))

print ("pred moving after scaling:")

print (preds_moving)

return preds_moving

print ("do moving test predictions for next 22 days:")

preds_moving = moving_test_window_preds(22)

count_correct=0

error =0

for i in range (len(y_test)):

error=error + ((y_test[i]-preds_moving[i])**2) / y_test[i]

if y_test[i] >=0 and preds_moving[i] >=0 :

count_correct=count_correct+1

if y_test[i] < 0 and preds_moving[i] < 0 :

count_correct=count_correct+1

accuracy_in_change = count_correct / (len(y_test) )

plt.figure(4)

plt.title("Forecast vs Actual, (data is differenced)")

plt.plot(preds_moving, label="predictions")

plt.plot(y_test, label="actual")

plt.legend(loc='upper center', bbox_to_anchor=(0.5, -0.05),

fancybox=True, shadow=True, ncol=2)

print ("accuracy_in_change:")

print (accuracy_in_change)

ind=data_original.index.values[0] + data_original.shape[0] -len(y_test)-1

prev_starting_price = data_original.loc[ind,"yt_"]

preds_moving_before_diff = [0 for x in range(len(preds_moving))]

for i in range (len(preds_moving)):

if (i==0):

preds_moving_before_diff[i]=prev_starting_price + preds_moving[i]

else:

preds_moving_before_diff[i]=preds_moving_before_diff[i-1]+preds_moving[i]

y_test_before_diff = [0 for x in range(len(y_test))]

for i in range (len(y_test)):

if (i==0):

y_test_before_diff[i]=prev_starting_price + y_test[i]

else:

y_test_before_diff[i]=y_test_before_diff[i-1]+y_test[i]

plt.figure(5)

plt.title("Forecast vs Actual (non differenced data)")

plt.plot(preds_moving_before_diff, label="predictions")

plt.plot(y_test_before_diff, label="actual")

plt.legend(loc='upper center', bbox_to_anchor=(0.5, -0.05),

fancybox=True, shadow=True, ncol=2)

plt.show()

In this post I will share experiment with Time Series Prediction with LSTM and Keras. LSTM neural network is used in this experiment for multiple steps ahead for stock prices data. The experiment is based on the paper [1]. The authors of the paper examine independent value prediction approach. With this approach a separate model is built for each prediction step. This approach helps to avoid error accumulation problem that we have when we use multi-stage step prediction.

LSTM Implementation

Following this approach I decided to use Long Short-Term Memory network or LSTM network for daily data stock price prediction. LSTM is a type of recurrent neural network used in deep learning. LSTMs have been used to advance the state-of the-art for many difficult problems. [2]

For this time series prediction I selected the number of steps to predict ahead = 3 and built 3 LSTM models with Keras in python. For each model I used different variable (fit0, fit1, fit2) to avoid any “memory leakage” between models.

The model initialization code is the same for all 3 models except changing parameters (number of neurons in LSTM layer)

The architecture of the system is shown on the fig below.

Multiple step prediction with separate neural networks

Here we have 3 LSTM models that are getting same X input data but different target Y data. The target data is shifted by number of steps. If model is forecasting the data stock price for day 2 then Y is shifted by 2 elements.

This happens in the following line when i=1:

yt_ = yt.shift (-i - 1 )

The data were obtained from stock prices from Internet.

The number of unit was obtained by running several variations and chosen based on MSE as following:

if i==0:

units=20

batch_size=1

if i==1:

units=15

batch_size=1

if i==2:

units=80

batch_size=1

If you want run more than 3 steps / models you will need to add parameters to the above code. Additionally you will need add model initialization code shown below.

Each LSTM network was constructed as following:

if i == 0 :

fit0 = Sequential ()

fit0.add (LSTM ( units , activation = 'tanh', inner_activation = 'hard_sigmoid' , input_shape =(len(cols), 1) ))

fit0.add(Dropout(0.2))

fit0.add (Dense (output_dim =1, activation = 'linear'))

fit0.compile (loss ="mean_squared_error" , optimizer = "adam")

fit0.fit (x_train, y_train, batch_size =batch_size, nb_epoch =25, shuffle = False)

train_mse[i] = fit0.evaluate (x_train, y_train, batch_size =batch_size)

test_mse[i] = fit0.evaluate (x_test, y_test, batch_size =batch_size)

pred = fit0.predict (x_test)

pred = scaler_y.inverse_transform (np. array (pred). reshape ((len( pred), 1)))

# below is just fo i == 0

for j in range (len(pred)) :

prediction_data[j] = pred[j]

For each model the code is saving last forecasted number.

Additionally at step i=0 predicted data is saved for comparison with actual data:

prediction_data = np.asarray(prediction_data)

prediction_data = prediction_data.ravel()

# shift back by one step

for j in range (len(prediction_data) - 1 ):

prediction_data[len(prediction_data) - j - 1 ] = prediction_data[len(prediction_data) - 1 - j - 1]

# combine prediction data from first model and last predicted data from each model

prediction_data = np.append(prediction_data, forecast)

The full python source code for time series prediction with LSTM in python is shown here

Below is the graph of actual data vs data testing data, including last 3 stock data prices from each model.

Multiple step prediction – actual data vs predictions

Accuracy of prediction 98% calculated for last 3 data stock prices (one from each model).

The experiment confirmed that using models (one model for each step) in multistep-ahead time series prediction has advantages. With this method we can adjust parameters of needed LSTM for each step. For example, number of neurons for i=2 was modified to decrease prediction error for this step. And it did not affect predictions for other steps. This is one of machine learning techniques for stock prediction that is described in [1]

You must be logged in to post a comment.